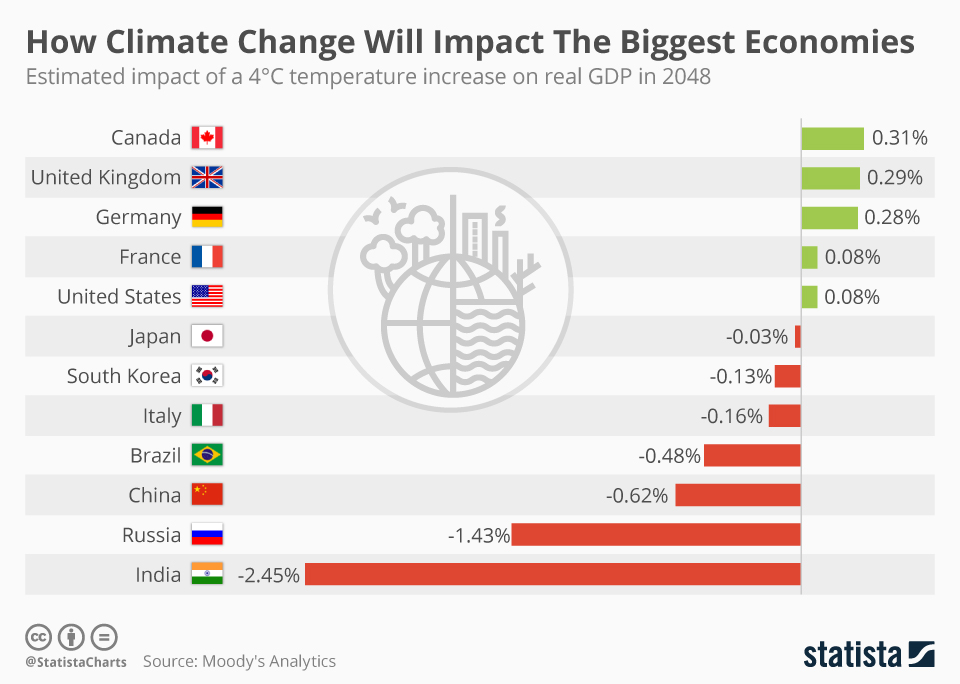

The economic impacts of climate change are poised to become a defining challenge of our time, with new studies indicating that these effects could be six times more severe than previously thought. With rising global temperatures coinciding with increased extreme weather events, macroeconomists have begun to reassess the potential repercussions on global GDP, predicting significant losses tied to each incremental degree of warming. The latest climate change forecasts suggest that a 1°C rise could result in a staggering 12 percent decline in economic output worldwide, emphasizing the urgency for effective decarbonization policies. As nations grapple with these economic consequences of climate change, the conversation surrounding environmental economics and sustainable growth becomes ever more critical. Ultimately, addressing these challenges not only protects our environment but also ensures lasting economic stability for future generations.

The repercussions of global warming extend far beyond environmental degradation, affecting economic stability and growth worldwide. As we witness increasingly erratic weather patterns and rising sea levels, policymakers and economists alike are beginning to connect the dots between climate instability and the forecasted downfall of once-thriving businesses and industries. Analysts have increasingly noted that the climate crisis poses urgent threats to national productivity, prompting the need for significant shifts in financial practices and investment in green technologies underpinned by robust environmental economics. By understanding the intricate interplay between climate patterns and economic performance, we can develop more effective strategies to mitigate global GDP loss and strengthen our resilience in the face of these pressing challenges.

Understanding the Economic Impacts of Climate Change

Climate change poses significant threats to global economies, as recent studies reveal economic impacts projected to be six times larger than previously estimated. The alarming consensus among climate scientists is that rising temperatures will lead to drastic reductions in productivity and GDP. Specifically, each additional 1°C increase in global temperature is expected to result in a staggering 12 percent decrease in global GDP, which emphasizes the urgency of addressing the economic consequences of climate change. This stark reality presents a pressing call for policymakers and businesses alike to acknowledge the severity of these forecasts and begin implementing effective mitigation strategies.

Furthermore, the complex interplay between economic growth and climate change complicates the forecasts. As macroeconomists explore their methodologies, they find that traditional estimates have often underestimated the compounded effects of global warming. With more extreme weather events linked to rising temperatures, capital and productivity losses will likely escalate. Thus, understanding the economic impacts of climate change is pivotal to ensure future resilience against its inevitable consequences.

Recent trends indicate that as global temperatures rise, we can expect not only a decline in productivity but also an increase in socio-economic disparities. Vulnerable populations are often at higher risk of experiencing job losses and decreased economic opportunities due to environmental disruptions. By addressing these issues through the lens of environmental economics, researchers can advocate for policies that alleviate these disparities while also protecting the broader economy. Ignoring the looming threats posed by climate change could cost economies dearly in terms of both human capital and resource allocation.

In conclusion, the economic repercussions of climate change are not merely theoretical projections but pressing realities that require immediate action. Policymakers and businesses should focus on sustainable practices and invest in innovative technologies to mitigate these impacts. As the evidence mounts regarding the economic consequences, it is imperative to acknowledge these findings to safeguard our economies against the disastrous effects of climate change.

The Role of Decarbonization Policies in Mitigating Economic Losses

Decarbonization policies emerge as a critical player in mitigating the adverse economic impacts of climate change. Recent studies suggest that targeted interventions can significantly reduce the social cost of carbon, making it a more viable option for countries aiming to transition towards a low-carbon economy. For instance, the social cost per ton of carbon dioxide emissions calculated at $1,056 by recent research starkly contrasts with previous estimations based solely on local temperature variations, which were significantly lower. This emphasizes the need to adopt comprehensive policies aimed at reducing greenhouse gas emissions to curtail future economic losses.

Furthermore, investing in decarbonization can yield positive economic outcomes that outweigh implementation costs. For large economies such as the U.S. and members of the European Union, transitioning to sustainable energy sources and facilitating green technologies can result in enhanced economic resilience. The findings of the recent study underscore that the costs associated with federal decarbonization measures, such as those outlined in the Inflation Reduction Act, are significantly lower than the social costs associated with inaction. This positions decarbonization not just as an environmental imperative but also as a crucial economic strategy.

The economic benefits of transitioning to a greener economy extend beyond immediate cost savings; they encompass job creation in renewable energy sectors and the promotion of technological innovation. By fostering cleaner industries, countries can achieve sustainable growth while addressing the impacts of climate change. The current forecasts indicate that while climate change may hinder potential economic growth, proactive decarbonization efforts can lead to better scenarios, with economies potentially growing faster than they would under a business-as-usual approach.

In summary, decarbonization policies are not merely an environmental necessity but an integral component of economic strategy. As nations consider their future paths in light of climate change’s stark realities, embracing sustainable practices can provide both resilience against economic challenges and opportunities for growth.

Exploring Climate Change Forecasts and Their Economic Implications

Climate change forecasts play a pivotal role in understanding the long-term economic implications of rising global temperatures. Recent analyses indicate that macroeconomic models have often underestimated the severity of these forecasts, leading to a dangerously complacent narrative about climate impacts. For example, changes in climate are expected to reduce productivity and GDP significantly—findings that have prompted economists to reconsider how they assess these forecasts. With a proposed 50 percent decline in output and consumption if temperatures rise an additional 2°C by century’s end, the stakes are high, necessitating a closer examination of climate science and its economic ramifications.

As researchers continue to refine their methodologies, it becomes clear that the complexity of climate change must be reflected in economic models. Traditional approaches that focus solely on local temperature variations fail to account for the broader impact of extreme weather events, a critical component of 21st-century climate realities. Consequently, an accurate understanding of climate change forecasts is essential for formulating policies that can effectively mitigate economic losses, enhance resilience, and promote sustainable growth in the face of increasing environmental challenges.

Long-Term Economic Consequences of Climate Change

The long-term economic consequences of climate change present a multifaceted challenge for global economies. With rising temperatures threatening agricultural productivity, altering trade patterns, and increasing the frequency of extreme weather events, the potential for long-term economic instability is substantial. Recent studies indicate that the approach of estimating GDP losses by correlating temperature increases provides a more comprehensive understanding of these impacts. As the temperature continues to rise, the cumulative effects on global GDP may echo for generations, hinting at a profound reshaping of economic landscapes across the globe.

Moreover, the implications of a warming planet extend beyond mere economic numbers and touch upon social equity and development issues. Economies may still experience growth, but the rate of inequality could also rise, leaving marginalized groups vulnerable to job losses and reduced access to essential services. This underscores the need to not only address the numerical estimates of GDP loss but to integrate social considerations into climate policies. Ensuring that growth is equitable in the face of climate challenges is essential for a resilient future.

Investigating the long-term economic consequences of climate change also reveals the importance of proactive measures in economic planning. Governments and businesses must account for environmental risks within their forecasting models, which can lead to more informed decision-making regarding investments and resource allocation. By incorporating climate change forecasts into economic strategies, countries can better safeguard against potential losses and bolster their adaptive capacity.

In summary, the long-term economic consequences of climate change are expansive and far-reaching. As we continue to confront these challenges, it is crucial to integrate climate considerations into economic analysis and decision-making. Failure to prepare for these long-term impacts could result in inadequate responses that worsen both economic and social disparities globally.

Reevaluating Methodologies for Climate Change Economic Analysis

The growing urgency surrounding the financial implications of climate change necessitates a reevaluation of traditional methodologies used in economic analysis. Researchers have found that existing models often overlook significant factors, such as the correlation between temperature increases and the frequency of extreme weather events. By employing innovative approaches that consider global temperature changes, economists can better estimate potential losses in GDP and provide a more accurate picture of future scenarios.

This effort to refine methodologies is crucial for effective policy-making. Traditional economic forecasts have sometimes downplayed the scale of potential economic loss associated with climate change, which has hampered the urgency needed to implement impactful decarbonization policies. By adopting a more comprehensive framework that accurately reflects the realities of climate science and its impacts on economies, stakeholders can prioritize investments in sustainable practices and technologies that not only mitigate greenhouse gas emissions but also bolster economic resilience.

For instance, integrating long-term climate data into economic models allows for a clearer understanding of the direct relationships between temperature changes and economic performance. This clarity can drive better resource management and targeting for funding projects aimed at enhancing resilience against extreme weather events. Policymakers must recognize that shifting to these enhanced methodologies will yield a more precise understanding of the costs and benefits associated with addressing climate change head-on.

In conclusion, reevaluating methodologies for climate change economic analysis is pivotal in crafting informed policies that can effectively mitigate the negative impacts predicted by climate forecasts. As we strive toward a sustainable future, aligning economic analysis with climate science will be vital to fostering a robust economy capable of enduring the challenges posed by a warming world.

The Importance of Sustainable Practices for Economic Resilience

Adopting sustainable practices has become imperative for enhancing economic resilience in the face of climate change. As temperatures rise and extreme weather events become more frequent, integrating sustainability into economic planning can help communities better prepare for potential shocks. This includes transitioning to renewable energy sources, implementing efficient resource management, and promoting sustainable agriculture practices. These approaches not only mitigate the adverse effects of climate change but also create opportunities for economic growth and innovation.

For businesses, embracing sustainable practices can yield competitive advantages. Companies that prioritize eco-friendly operations are increasingly attracting environmentally conscious consumers, leading to enhanced brand loyalty and market share. Additionally, sustainable initiatives can reduce operational costs through energy efficiency and waste reduction, contributing to the bottom line while simultaneously addressing global warming. Thus, businesses that leverage sustainability as part of their growth strategy will likely fare better in an increasingly climate-conscious market.

Moreover, investments in sustainable practices can bolster job creation and economic development. The shift towards a green economy fosters new industries and employment opportunities, ranging from renewable energy to sustainable agriculture. Communities that embrace these changes can benefit economically while simultaneously enhancing their resilience to climate impacts. As demonstrated by emerging research, the economic gains from sustainable initiatives significantly outweigh the costs, further demonstrating the feasibility of integrating sustainability into economic frameworks.

In summary, the importance of sustainable practices for economic resilience against climate change cannot be overstated. By investing in renewable energy and environmentally friendly practices, economies can better adapt to the challenges posed by a changing climate while reaping considerable economic rewards.

Frequently Asked Questions

What are the economic impacts of climate change on global GDP projections?

Recent studies indicate that the economic impacts of climate change could result in a 12% reduction in global GDP for every additional 1°C rise in temperature. This forecast suggests that the economic consequences of climate change are significantly more severe than previously estimated, with potential losses peaking within six years after temperature increases.

How do climate change forecasts affect future economic growth?

Climate change forecasts reveal that while future economic growth may continue, the detrimental effects of rising temperatures could lead to a substantial decline in output and consumption. For instance, a projected 2°C increase in global temperatures by 2100 could halve economic output, highlighting the critical economic impacts of climate change.

What methodologies are used to assess the economic consequences of climate change?

To assess the economic consequences of climate change, researchers utilize complex models that examine temperature variations and their impacts on productivity. These methods aim to control for factors like technological growth to offer accurate climate change forecasts related to economic performance.

What role do decarbonization policies play in mitigating the economic impacts of climate change?

Decarbonization policies are essential in addressing the economic impacts of climate change. Research has shown that effective decarbonization can provide significant economic benefits, surpassing costs, as observed in analyses of large economies like the EU and U.S., making it a wise investment against projected climate-related GDP losses.

What is the social cost of carbon and how does it relate to the economic impacts of climate change?

The social cost of carbon quantifies the economic damage associated with CO2 emissions. Recent estimates suggest a social cost of $1,056 per ton globally, far exceeding earlier assessments. This measure is crucial for creating effective decarbonization policies that can alleviate the economic impacts of climate change by encouraging lower emissions.

How do extreme weather events influence the economic impacts of climate change?

Extreme weather events, which increase in frequency with rising global temperatures, severely impact productivity and economic stability. The correlation between global temperature increases and extreme weather events underscores the urgency of addressing the economic consequences of climate change to protect future growth.

| Key Point | Details |

|---|---|

| New Economic Estimates | The economic impacts of climate change are projected to be six times larger than previous estimates based on a new study. |

| Projected GDP Loss | A 1°C increase in global temperatures is estimated to lead to a 12% reduction in global GDP, peaking six years after the temperature rise. |

| Previous Methodology Issues | Past economic forecasts have underestimated the impacts, often ignoring extreme weather events and focusing only on local temperature changes. |

| Extreme Weather Correlation | Global temperature increases are linked not only to heat waves but also to increased incidents of severe weather—important for economic modeling. |

| Future Projections | An additional 2°C rise by 2100 could lead to a 50% decline in output and consumption, a severe scenario compared to the Great Depression. |

| Social Cost of Carbon | Using new methods, the social cost of carbon was estimated at $1,056 per ton globally, significantly higher compared to previous estimates. |

| Decarbonization Viability | The economic analysis supports decarbonization policies, showing they can have positive cost-benefit outcomes, especially for large economies. |

Summary

The economic impacts of climate change represent a significant threat to global prosperity, far exceeding earlier predictions. Recent studies highlight that every 1°C increase in temperature could result in a staggering 12% decrease in global GDP. Furthermore, projections indicate that a rise of an additional 2°C by the end of the century could reduce output and consumption by as much as 50%. Despite economic growth continuing, the overall wealth could be hindered compared to a world without climate issues. While challenges in evaluating these economic impacts remain, the urgency for effective decarbonization strategies is clear, as they could prove beneficial for large economies like the U.S. and the European Union, making it imperative to prioritize climate action.